Certified Financial Planner Alexa von Tobel Answers 4 Money FAQs

Q&A with Organizational Pro Peter Walsh + Dermatologist Shares A…

Actor Hank Azaria + Freezer Meals + Artichokes 2 Ways with Rach

See Inside Barbara Corcoran's Stunning NY Apartment + It's Steak…

How to Make Chicken and Lobster Piccata | Richard Blais

Donnie Wahlberg Spills Details About NKOTB's First Ever Conventi…

Donnie Wahlberg + Jenny McCarthy Say Rach Is Such a "Joy" + Look…

The Best Moments From 17 Seasons of the Show Will Make You Laugh…

How to Make Crabby Carbonara | Rachael Ray

Rach Chats "Firsts" In Flashback From Our First Episode Ever In …

How to Make Apple-Cider Braised Pork Chop Sandwiches with Onion …

Rach's Chef Pals Say Goodbye to Show in Surprise Video Message

How to Make Sesame Cookies | Buddy Valastro

How to Make Tortilla with Potatoes, Piquillo Peppers and Mancheg…

How to Make Shrimp Burgers | Jacques Pepin

How to Make Spanakopipasta | Rachael Ray

Andrew McCarthy Chokes Up Discussing Emotional Trip to Spain wit…

Celebrity Guests Send Farewell Messages After 17 Seasons of the …

Celebrity Guests Send Farewell Messages After 17 Seasons of the …

Andrew McCarthy Teases Upcoming "Brat Pack" Reunion Special

Michelle Obama Toasts Rach's 17 Years on the Air With a Heartfel…

Alexa von Tobel is the founder and CEO of LearnVest and author of the new book, Financially Forward — so when she gives money advice, we listen!

What does being financially forward mean to Alexa? "For me, being financially forward is about helping people," she says. "It's 2019 — we want to make sure that you use all the technology that exists — but also keep to basic, practical financial advice."

Her goal is to make money management accessible to everyone, no matter their income or status. And as a certified financial planner (CFP), there are some common questions Alexa says she is asked all the time.

Alexa shared her top four FAQs about finances with us, along with her expert advice.

1. Should I merge my finances with my partner's?

One of the biggest questions the CFP gets is from couples who are getting engaged, asking if (and how) they should merge their finances.

According to Alexa, there are three possible ways you can go about it.

You can do nothing and keep your finances separate, although she wouldn't recommend going this route.

The second option is combining ALL of your finances, but Alexa says many people aren't comfortable with this either.

Lastly — and this seems to be Alexa's preference — you can follow what she calls the "hybrid model," which means having three separate categories: "Yours," "Mine," and "Ours."

"Let's say one person makes $100,000 and one person makes $50,000," Alexa says, "you would take 75% and put it in your joint [account]."

That "ours" money — which is 75% of your total combined incomes (so in this example it would be $112,500) — should be put toward rent, groceries and everything you pay for together as a couple.

Then, each of you should put the remaining 25% of your take-home pay into your own personal accounts (i.e. $25,000 for the first person and $12,500 for the second). That way, if you want to have an extra glass of wine with a friend or buy a gift for your significant other, you don't have to feel obligated to ask your partner for permission to take the money out of your shared account.

"This hybrid approach is a very good way for people to start joining their finances," Alexa says.

RELATED: Should Spouses Have a Joint Bank Account? Married Couple Rev Run + Justine Simmons Answer

2. Should I pay off my credit card debt or contribute to my 401(k) first?

If you have a lot of credit card debt, it can be difficult to know whether you should prioritize that, or prioritize contributing to your 401(k).

Here's the answer: If your company has 401(k) matching (that means they're giving you FREE MONEY), you should do both. "Pay off your credit card debt and take full advantage of that match," Alexa says.

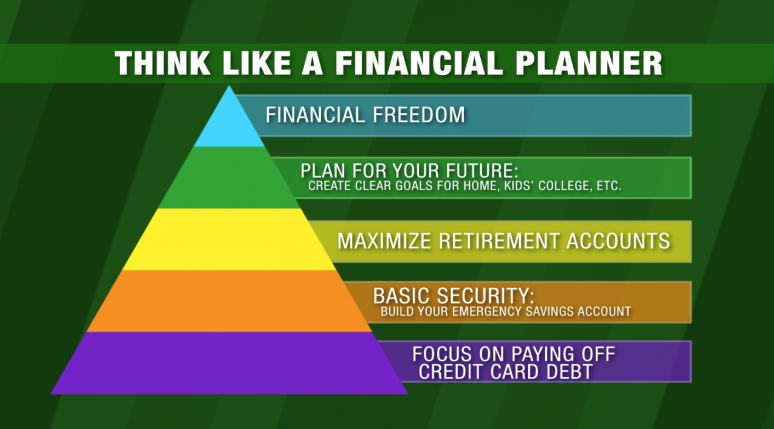

But if you're still confused about what to tackle first, Alexa suggests using this handy pyramid:

Rachael Ray Show

The pyramid is organized in order of importance, with the bottom of the pyramid being the most important — A.K.A. where you should begin. So, you want to focus first on paying off any credit card debt you may have. (According to Alexa, the average American has a lot of credit card debt — there's no judgment, but it is crucial to your financial health to take care of it as soon as possible.)

Next up is basic security, or "having an emergency savings account, which we all need," Alexa continues.

"How many months does emergency translate to, minimum?" Rach asks.

Alexa says determining the necessary liquid savings you should have is simple: If you're young and single, it's three months, if you're married with a mortgage it's sixth months and once you have kids, it's nine to 12 months, she explains.

Then comes saving for the future, specifically maximizing your retirement accounts: your 401(k) and your IRA.

And finally, all the fun stuff — planning for your future! This means thinking about saving for a home, a vacation, a house renovation or another big future expense.

Once you get to the top of the pyramid, you're financially free. "This is when you get to start living a more fluid financial life, because everything below it is taken care of," the financial expert says.

3. How do I know if I have enough money to buy a house?

People like to say, "It's a buyer's market." But what does that really mean? How do you know when to start thinking about buying a home, and how will you know when you're actually financially ready to buy?

Here are Alexa's rules, so that you don't end up getting tricked into spending more money than you should:

First, do your research. Go online and get a general sense of what you're looking for and how much it should cost.

Then, know that you need to have 20% ready to put down — this is a non-negotiable number, according to Alexa. So if the home is $300,000, that's $60,000 a CFP would want you to have set aside for this specific purchase.

Watch the video above to see Alexa explain how to calculate your savings goal (per month), based on the cost of the house and how soon you'd like to buy it.

4. Should I use a 0% APR credit card?

If you have a lot of credit card debt and you're wondering if you should apply for a 0% APR credit card to pay off that debt, the simple answer is yes, Alexa says.

(APR stands for annual percentage rate, and it keeps you from accruing further interest charges for a certain period of time.)

You can do a balance transfer ONE time per year, the CFP explains — any more and you risk damaging your credit score.

"But after 6 months, that 0% APR skyrockets," she says. "You can only do it as long as you can actually pay off that credit card debt in six months." (A.K.A. don't charge anything to that new card — only use it to tackle existing debt!)